Penetration of new international markets, and the application of the flywheel distribution model are the foundation Klappir expects to build its growth upon. With AI layered on top of the system, customers will find wins easily, increasing retention and ACV for Klappir

With accelerated revenue growth and the high operating leverage enabled by the distribution model and AI advancements, reported EBITDA margin is projected to expand to 43.7% by 2030. Net of capitalization the EBITDA margin is projected to be 19.1%.

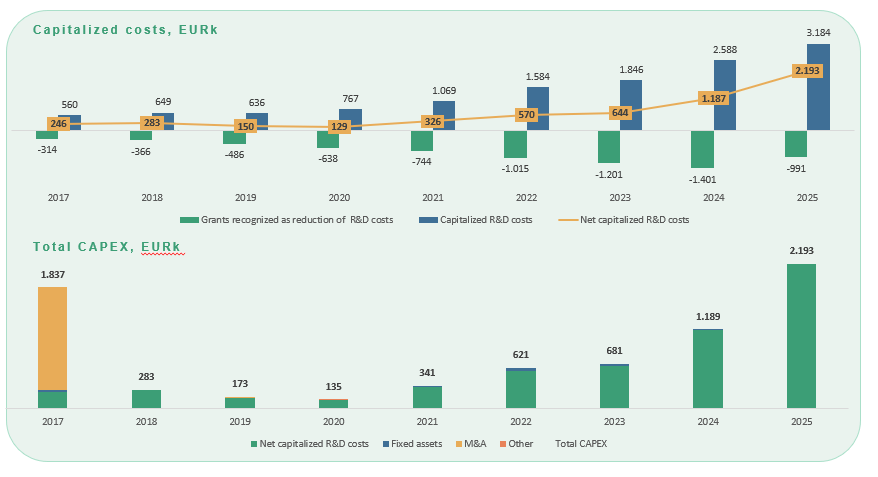

From 2026-2030, investments in business development efforts to realize the growth plan are expected. These costs are often not eligible for capitalization. Capitalization as a % of revenue is thus expected lower, reflecting a shift from a building phase to the growth phase. No grants are included in the forecast.